All Categories

Featured

Table of Contents

- – What is Level Benefit Term Life Insurance? A S...

- – How Does Term Life Insurance Level Term Protec...

- – What is Direct Term Life Insurance Meaning? D...

- – All About What Does Level Term Life Insurance...

- – How Does Level Term Life Insurance Meaning P...

- – What is 10-year Level Term Life Insurance? F...

If George is diagnosed with a terminal ailment throughout the very first plan term, he probably will not be qualified to renew the plan when it runs out. Some policies supply ensured re-insurability (without proof of insurability), but such attributes come at a greater price. There are a number of types of term life insurance policy.

Normally, most business use terms ranging from 10 to thirty years, although a few deal 35- and 40-year terms. Level-premium insurance policy has a set regular monthly payment for the life of the plan. Many term life insurance policy has a degree premium, and it's the type we've been describing in many of this write-up.

Term life insurance policy is attractive to youths with youngsters. Parents can acquire significant coverage for an affordable, and if the insured passes away while the plan is in impact, the family members can depend on the fatality benefit to replace lost income. These plans are likewise fit for individuals with growing family members.

What is Level Benefit Term Life Insurance? A Simple Explanation?

Term life plans are ideal for individuals that want significant protection at a reduced price. People who own whole life insurance policy pay extra in costs for much less insurance coverage but have the safety of recognizing they are protected for life.

The conversion biker should permit you to transform to any permanent policy the insurance policy company offers without limitations. The primary functions of the biker are keeping the original health rating of the term plan upon conversion (also if you later on have wellness problems or come to be uninsurable) and determining when and just how much of the protection to transform.

Naturally, overall costs will raise substantially considering that whole life insurance policy is much more costly than term life insurance policy. The benefit is the guaranteed authorization without a medical examination. Medical conditions that create throughout the term life period can not create costs to be boosted. The company may call for limited or complete underwriting if you want to include extra motorcyclists to the brand-new policy, such as a long-lasting treatment biker.

How Does Term Life Insurance Level Term Protect Your Loved Ones?

Term life insurance policy is a fairly affordable method to offer a lump amount to your dependents if something occurs to you. It can be a good choice if you are young and healthy and balanced and sustain a family members. Whole life insurance policy comes with considerably greater monthly premiums. It is suggested to give insurance coverage for as lengthy as you live.

It relies on their age. Insurer set a maximum age limit for term life insurance policies. This is usually 80 to 90 years old but may be higher or reduced relying on the company. The costs additionally increases with age, so an individual matured 60 or 70 will certainly pay considerably more than somebody years younger.

Term life is rather similar to cars and truck insurance. It's statistically unlikely that you'll need it, and the costs are money down the drainpipe if you don't. If the worst happens, your household will obtain the benefits.

What is Direct Term Life Insurance Meaning? Detailed Insights?

For the a lot of part, there are two kinds of life insurance policy strategies - either term or irreversible strategies or some combination of the 2. Life insurance companies offer numerous kinds of term plans and conventional life policies along with "interest delicate" items which have actually ended up being more prevalent because the 1980's.

Term insurance offers protection for a specific time period. This duration could be as brief as one year or provide insurance coverage for a specific number of years such as 5, 10, 20 years or to a specified age such as 80 or in some cases up to the oldest age in the life insurance coverage mortality.

All About What Does Level Term Life Insurance Mean Coverage

Presently term insurance policy prices are really competitive and amongst the least expensive traditionally experienced. It needs to be kept in mind that it is a widely held belief that term insurance is the least pricey pure life insurance policy coverage readily available. One requires to evaluate the plan terms very carefully to make a decision which term life alternatives appropriate to meet your particular circumstances.

With each new term the costs is raised. The right to restore the policy without proof of insurability is an important benefit to you. Or else, the threat you take is that your health and wellness may weaken and you might be incapable to obtain a plan at the same prices or even in any way, leaving you and your recipients without coverage.

You need to exercise this choice during the conversion duration. The length of the conversion duration will vary relying on the sort of term policy purchased. If you transform within the proposed period, you are not required to give any kind of information regarding your wellness. The costs price you pay on conversion is usually based on your "present obtained age", which is your age on the conversion date.

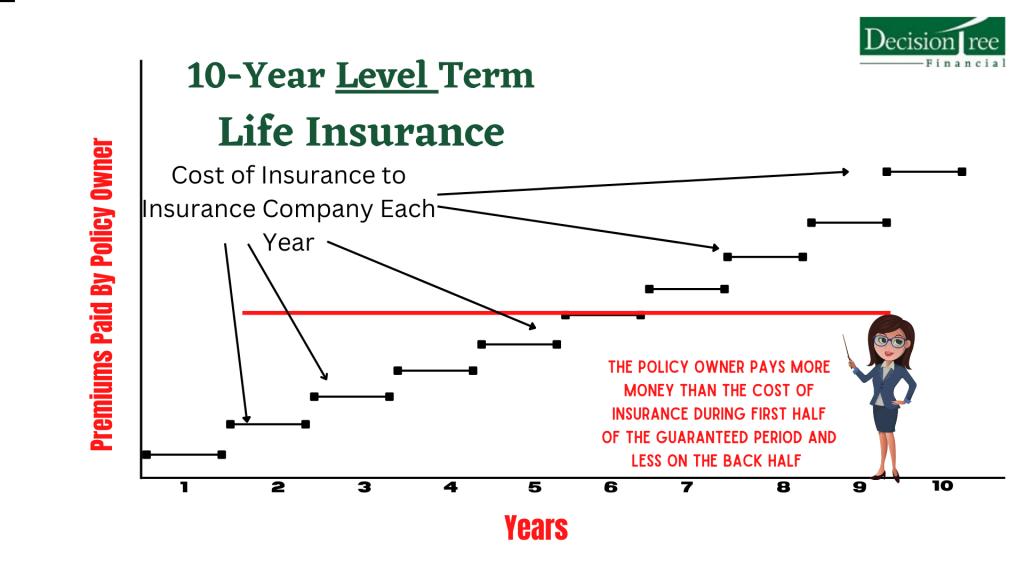

Under a level term plan the face quantity of the policy continues to be the exact same for the whole duration. With decreasing term the face quantity lowers over the period. The costs stays the exact same yearly. Commonly such plans are marketed as home loan protection with the quantity of insurance lowering as the balance of the mortgage decreases.

Commonly, insurance companies have actually not can transform costs after the plan is sold. Given that such plans may proceed for several years, insurance providers should utilize traditional death, rate of interest and expense price estimates in the costs estimation. Flexible costs insurance coverage, nevertheless, allows insurance companies to supply insurance policy at lower "current" premiums based upon less traditional presumptions with the right to change these costs in the future.

How Does Level Term Life Insurance Meaning Protect You?

While term insurance policy is designed to give security for a specified time period, irreversible insurance is created to supply insurance coverage for your whole life time. To keep the premium rate degree, the premium at the younger ages surpasses the actual cost of defense. This additional costs develops a get (cash money value) which helps pay for the plan in later years as the expense of defense increases over the premium.

The insurance policy company spends the excess costs bucks This type of policy, which is occasionally called cash value life insurance coverage, creates a financial savings element. Cash worths are vital to a permanent life insurance policy.

Sometimes, there is no connection between the size of the money worth and the premiums paid. It is the money value of the policy that can be accessed while the policyholder lives. The Commissioners 1980 Criterion Ordinary Mortality Table (CSO) is the existing table used in determining minimal nonforfeiture values and plan books for common life insurance policy policies.

What is 10-year Level Term Life Insurance? Find Out Here

Many long-term plans will contain provisions, which specify these tax obligation needs. Standard whole life policies are based upon lasting estimates of cost, passion and mortality.

{kind=link}

Table of Contents

- – What is Level Benefit Term Life Insurance? A S...

- – How Does Term Life Insurance Level Term Protec...

- – What is Direct Term Life Insurance Meaning? D...

- – All About What Does Level Term Life Insurance...

- – How Does Level Term Life Insurance Meaning P...

- – What is 10-year Level Term Life Insurance? F...

Latest Posts

What Is The Difference Between Life And Burial Insurance

Final Expense Insurance Training

Online Funeral Cover Quotes

More

Latest Posts

What Is The Difference Between Life And Burial Insurance

Final Expense Insurance Training

Online Funeral Cover Quotes